Local vs. National Media Strategy: The Mistake Multi-Location Brands Keep Making

Most multi-location brands frame local and national media as a budget trade-off. That framing is the mistake, and it costs them efficiency every quarter they hold onto it.

If you run media across more than a handful of locations, you have sat in a budget meeting where someone asked the wrong question: "We can't afford both. Should we spend on national brand, or double down on local conversion?" The answer is no. The question is the problem, and brands that keep asking it pay more per acquired customer than those that have moved past it.

The Framing Problem That Costs Multi-Location Brands Millions

Local and national media do not compete for the same job. They occupy different positions in the same customer journey, and treating them as a trade-off breaks the loop that makes either work.

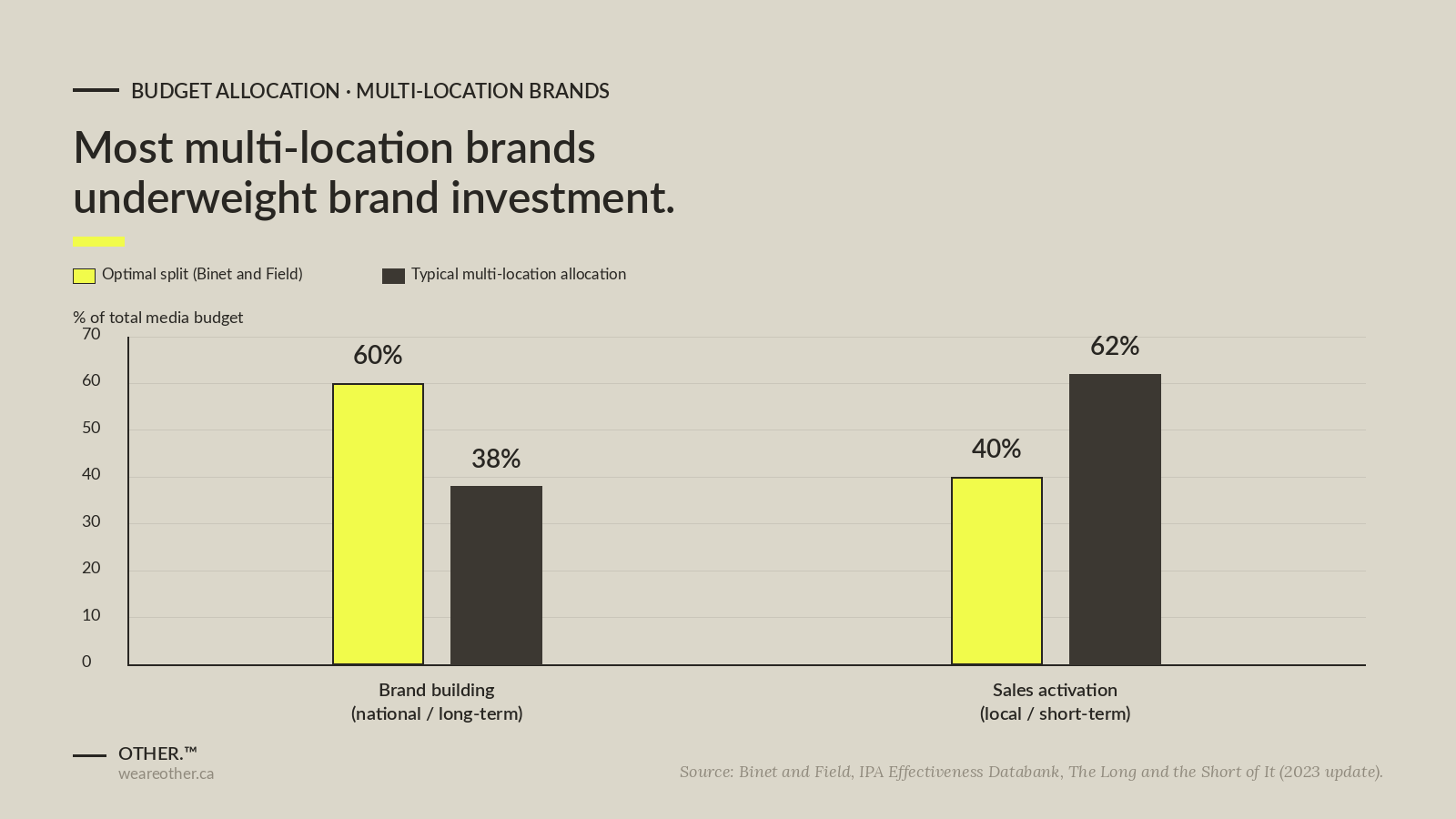

National media creates the conditions for local media to work. A consumer who has seen a brand's message three or four times before clicking a local paid search ad converts at a meaningfully higher rate than one who has not. Binet and Field's analysis of the IPA Effectiveness Databank found that the most effective campaigns split budget roughly 60% to brand building and 40% to sales activation. Brand investment compounds the short-term return on activation spend. Cutting national to fund local looks like a saving on the spreadsheet, and shows up as rising cost per acquired customer eighteen months later.

The second framing failure is conflating "local" with "small budget" and "national" with "brand awareness." Local campaigns in dense metros can be significant in scale, and national campaigns can drive direct response when built that way. The distinction is about audience specificity and the conversion intent of the moment you reach the consumer.

For franchise and multi-location home services brands, this failure shows up as persistent tension between corporate marketing (who control national spend) and local operators (who want more activation in their market). The solution is not more budget. It is clearer integrated media planning and an architecture that lets each layer of investment do its job.

Local and national are not competing budget lines. They are sequential jobs in the same customer journey, and brands that frame them as a choice pay for it in efficiency.

What National Media Actually Does (and Doesn't Do)

National media's primary job is trust at scale. Connected TV, programmatic display, streaming audio, and national publishers create the baseline of familiarity that makes every downstream touchpoint more efficient. When someone encounters a local paid search ad from a brand they have seen before, CPC efficiency improves and conversion rates rise. Google built its Search Lift and Conversion Lift frameworks precisely because standard conversion reports undercount upper-funnel video's impact on later search behavior.

National media is also the control layer for message consistency. Franchise systems and multi-location brands have a structural consistency problem: dozens of operators and sometimes dozens of agency relationships, all capable of drifting from brand standards in their own market.

What national media does not do well is convert in the moment. A consumer watching a connected TV ad for an HVAC brand at 9 PM is not booking a service call from the couch. Brands that judge brand investment by last-click cut it at exactly the wrong moment. Both the IAB and Nielsen have published work showing that brand campaigns measured on last-click attribution alone are systematically undervalued, often by a factor of two or more. Measure national media by its effect on downstream conversion rates, cost per acquired customer over a multi-quarter window, and the growth of branded search query volume in each market it touches.

National media's job is to make every downstream channel cheaper, not to win the last click. Measure it that way or stop investing in it.

What Local Media Actually Does (and Where It Breaks Down)

Local media's job is conversion. Geo-targeted paid search, location-specific paid social, Google Local Service Ads, and community-level placements turn awareness into intent and intent into a booked appointment. This is where unit economics get decided.

Local paid search is where most multi-location brands underinvest or execute badly. The tactical failure is almost always the same: city-level or metro-level targeting when the data supports neighborhood-level targeting. LocaliQ's 2025 home services benchmarks (compiled from WordStream data) show an average CPC of $7.85 for home services, with subcategories like Electricians ($12.18) and Roofing ($10.70) running higher. "HVAC repair Boston" and "HVAC repair South Boston" are different searches with different competitive dynamics and conversion economics. Treating them as one bucket means you cannot optimize either.

Local also breaks down when it runs without national support. In trust-sensitive categories like home services, financial services, and healthcare, a consumer's first interaction with a brand through a cold local search ad converts at a fraction of the rate of a warm one. This is the mechanism by which cutting national appears to save money in the short term and quietly destroys efficiency in the long one.

The second failure mode is local campaigns that get built, launched, and then never touched. Multi-location brands often have more active campaigns across more markets than their team can optimize. The budget keeps running against stale creative, drifting match types, and geo-targeting that no longer matches where customers actually live. Our performance media work most often starts here, because the savings from cleaning this up tend to fund the rest of the strategy.

Local converts only when the audience is warm and the targeting is precise. Cold local against city-level targeting is the most common waste in multi-location media.

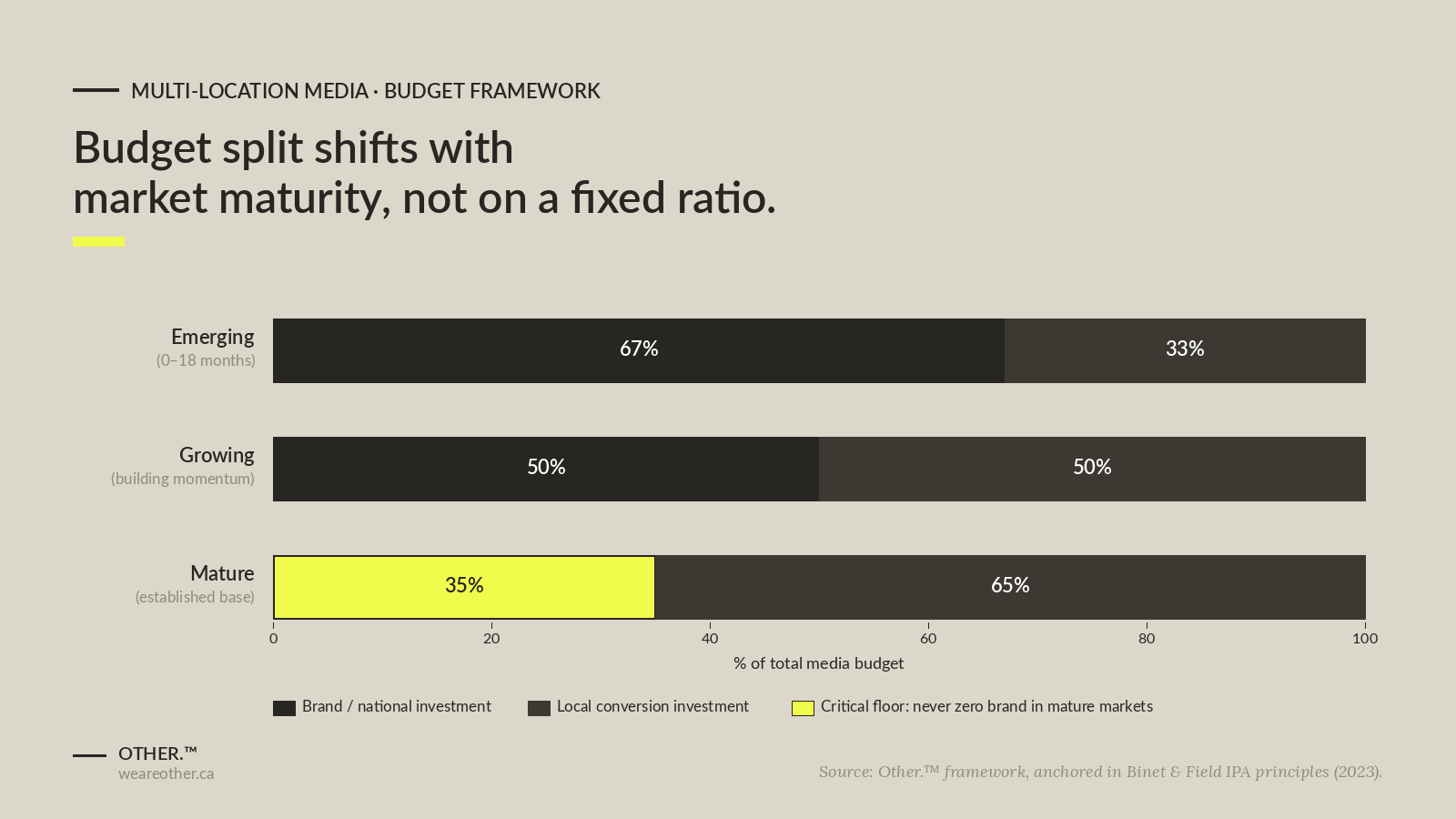

The Market Maturity Framework: How to Decide the Right Split

The right national-to-local ratio is not a universal benchmark. It is a function of where each market sits in its maturity cycle. Applying a single ratio across all locations is one of the most common sources of inefficiency in multi-location planning.

There are three stages, and the budget philosophy changes in each:

- Emerging markets (launched within 12 to 18 months, low brand recognition): weight 65% to 70% of spend toward brand and awareness. Local conversion should run at 30% to 35%, with lower conversion rates expected until brand recognition builds. Investing heavily in local too early produces high CPL and frustrates operators.

- Growing markets (established presence, building momentum): move toward a 50/50 split. Brand investment maintains the trust baseline. Local campaigns can now be optimized against a growing body of location-level data, where geo-targeting refinement produces the most improvement.

- Mature markets (high brand recognition, established customer base): shift 60% to 70% toward local conversion and retention. National brand should never go to zero; brands that abandon awareness in mature markets create vulnerability to new entrants. The return on incremental local spend is highest here, but the brand floor has to hold.

The mistake most brands make is assigning budgets annually by location without re-evaluating market stage. A location that was emerging two years ago may now be mature. Running a brand-heavy strategy against a mature market wastes money. Running a conversion-heavy strategy in an emerging one frustrates local operators and produces weak results. Both feel like a media problem. Both are a planning problem.

Re-grade every market at least annually against the three-stage framework, and budget against the stage you are in, not the stage you were in.

Why Campaign Architecture Matters More Than Channel Selection

Channel selection is almost never the primary driver of multi-location media performance. Architecture is. How campaigns are structured, how geo-targeting is set, how budgets are allocated at the location level, and how creative is versioned locally are the decisions that determine whether a channel produces results.

Geo-targeting precision is the most impactful architectural decision in local campaigns. City-level targeting in dense urban markets like New York, Boston, or the DC metro is structurally wasteful. It blends neighborhoods with different competitive dynamics, consumer profiles, and conversion economics into a single bucket that cannot be meaningfully optimized. Location-level or neighborhood-level targeting is the baseline requirement, not an advanced tactic.

Campaign architecture for franchise and multi-location brands also has to treat brand consistency as a non-negotiable parameter. Operators who run their own campaigns outside a centrally managed structure almost always drift from brand standards, create keyword cannibalization between adjacent locations, and produce attribution data that cannot be trusted at the network level.

The centralization model that works is one where corporate or a strategic media partner sets architecture, creative standards, geo-targeting parameters, and budget allocation. Individual locations execute within that framework, not outside it. This is not about removing local autonomy. It is about ensuring local campaigns strengthen rather than undercut the national investment making them work.

Architecture beats channel choice. The brands that win in multi-location media are not on different platforms; they run the same platforms better.

Measurement: The Part Most Agencies Skip

Single-touch attribution is not a viable measurement model for multi-location brands running integrated campaigns. Last-click systematically undervalues national media (which rarely gets the last click) and overstates the value of local paid search (which often does). Nielsen's 2024 Annual Marketing Report found that 50% of brands underinvest in media to achieve maximum ROI, and full-funnel measurement can improve overall ROI by 13% to 70%. Brands optimizing on last-click alone consistently cut the wrong spend.

The framework that actually works treats the journey as a sequence rather than a single event. Track the path from national exposure (impression data, brand lift studies, CTV reach) through mid-funnel engagement (branded search volume, direct traffic, return visit rates) to local conversion (geo-attributed leads, booked jobs, revenue by location). Each stage has its own KPIs and its own optimization logic.

At the location level, the metric that matters most is cost per acquired customer, not cost per lead, with local CPL benchmarked against the specific market rather than the national average. A $150 cost per lead in Manhattan may be excellent. The same $150 in a mid-sized Midwest market may signal something is structurally wrong.

AI referral traffic is now a measurable channel most multi-location brands are not yet tracking. Segment traffic from ChatGPT, Perplexity, and Google AI Mode from organic in Google Analytics 4. Brands building authority in these channels now are establishing a compounding advantage competitors will struggle to close.

Transparency in execution is the precondition for any of this to work. If a brand cannot see where every dollar in a local campaign is going (placements, geographies, creative versions), it cannot optimize. The ANA's 2023 Programmatic Media Supply Chain Transparency Study found that only 36 cents of every dollar entering a DSP effectively reaches the consumer; the rest goes to transaction costs, non-viewable impressions, and made-for-advertising waste. Hidden commissions and bundled fees make integrated measurement impossible regardless of how good the strategy looks on paper.

Last-click attribution will systematically destroy the wrong line items. Build sequence-based measurement or accept that you are optimizing in the dark.

What Good Integration Looks Like in Practice

Three scenarios drawn from situations multi-location CMOs often describe in a first meeting.

A home services franchise expanding into a new metro launches national CTV and programmatic display alongside branded paid search from day one. Branded search captures the demand the upper-funnel creates, since CTV exposure sends prospects to Google looking for the brand by name. Any spend not catching that traffic hands it to competitors bidding on the brand term. Local generic and competitive paid search layer in 60 to 90 days later, once branded search volume confirms awareness has built. Local campaigns target emergency and high-intent keywords at the neighborhood level. CPL in the first 90 days runs above the network average; by month six, conversion rates are within roughly 15% of mature-market benchmarks. The brand did not save money by skipping the brand build. They earned the savings on the back end.

An established franchise system loses efficiency in mature markets. CPL rises 18% year over year on flat budgets. An audit reveals city-level targeting in dense metros, keyword cannibalization between adjacent locations, and national brand cut 18 months earlier to fund expansion. The fix: restore national brand to roughly 30% of total, restructure local campaigns at the neighborhood level, and implement negative keyword sharing across locations. CPL stabilizes within two quarters.

A franchise operator is frustrated with the corporate model. Operators run independent campaigns alongside corporate-managed ones, creating keyword overlap that raises CPCs network-wide. Attribution is unreliable because conversions split across multiple tracking setups. The fix: consolidate management under a centralized structure with location-level reporting, give operators visibility into their own performance data, and set brand guardrails that permit local customization. None of those moves cost more.

Integration is not a creative decision or a budget decision. It is an architecture decision, made once and enforced quarterly.

Why It Matters

Four reasons this matters now:

- The math compounds. A 15% efficiency gain in year one becomes a structural advantage in year three. Brands that fix integration early stop competing on budget and start competing on system quality.

- Local operators see the work. Franchise councils trust media decisions they can verify. Transparent reporting at the location level turns operator skepticism into operator advocacy.

- The measurement gap is widening. Brands still optimizing on last-click are about to be three years behind those that have moved to sequence-based attribution.

- AI search is reshaping the demand layer. Multi-location brands building authority in AI-driven discovery now will be cited when consumers ask Perplexity or ChatGPT for a recommendation.

The brands compounding advantage in multi-location media are not the ones with the biggest budgets. They are the ones that stopped framing local and national as a competition.

Closing Guidance

What CMOs and senior marketers should do now:

- Audit the framing first. If your team is still debating local vs. national as a budget trade-off, the fix is the conversation, not the spend. Re-frame planning around customer journey stages.

- Grade every market. Build a three-stage classification of every market you operate in and revisit the grade annually. Budget against the grade, not last year's allocation.

- Pull the geo-targeting in. In dense metros, move from city-level to neighborhood or location-level targeting immediately. This single change typically reclaims 10% to 25% of wasted local search spend.

- Build a measurement stack that respects the journey. Stop optimizing on last-click. Layer brand-lift, mid-funnel engagement, and location-level CPA into one view, even if version one is imperfect.

- Demand transparency. If your media partner cannot show you where every dollar in a local campaign is going at the placement level, you cannot diagnose what is wrong. That is the precondition for everything above.

The bottom line: the brands that win in multi-location media are not the ones with the biggest budgets, they are the ones that built an architecture where local and national make each other work.

If you are looking at rising CPL in mature markets or planning an integrated launch into a new one, we are here to help.

Sources: Binet and Field (IPA Effectiveness Databank), LocaliQ/WordStream, IAB, Nielsen, ANA, Google Ads.

Let’s raise the bar together.